How pass-through voting works alongside fiduciary duty

Context

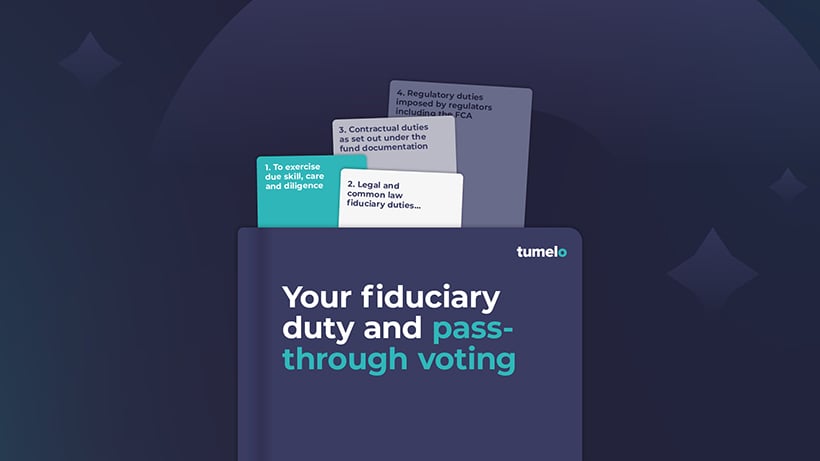

A fund manager's fiduciary duty comes from four sources:

- Tort being the tortious duty to exercise due skill, care and diligence.

- Legal and common law fiduciary duties imposed by the legal structure of the fund. For example, the board of directors of a fund with a company structure (like many ETFs) will have fiduciary duties under the Companies Act, 2006.

- Contractual duties as set out under a fund's documentation.

- Regulatory duties imposed by regulators such as the Financial Conduct Authority (FCA).

The FCA Handbook contains multiple requirements which are applicable to funds and fund managers. These vary - some are high-level principles, while some are detailed rules regarding funds.

The following FCA principles are relevant:

- Principle 2: A firm must conduct its business with due skill, care and diligence.

- Principle 3: A firm must pay due regard to the interests of its customers and treat them fairly.

Before pass-through voting, a fund manager would vote in a single direction to maximise the long-term returns of their fund. Moving forward, pass-through voting clearly creates a new opportunity for conflicting votes to be cast from within one fund.

How then does a fund manager ensure votes are being cast: i) fairly, and ii) with due skill, care, and diligence in the best interests of customers?

The new world of pass-through voting

Funds that are set up as companies (as is the case with many listed ETFs) have their own legal identity. Therefore, it is the company - not the underlying investor of the company - who owns the underlying assets (including shares), typically through a depositary/custodian. The investors in turn own shares in the company.

In a unit trust, the participants hold units of interests in a portfolio of assets, which is entrusted to a trustee. The management company (including the fund manager) is responsible for the selection of investments and administration of the fund, including voting.

With pass-through voting, the vote entitlement does not move from the company or the fund manager; even though either can choose to delegate the vote decision to the client. Because the entitlement does not move, the fund manager retains fiduciary responsibility for voting, as well as their existing requirements to report on stewardship activity.

Tumelo's platform offers several features that allow fund managers to enable pass-through voting while meeting their fiduciary duties.

Maintaining vote override

When funds are pooled, voting rights on the underlying securities belong to the fund (rather than the clients of the fund), which is its own legal entity.

However, there is a risk that if shareholders start voting on key matters, they could be considered as shadow directors and take on the personal liabilities that directors have for any breach of fiduciary duties. There is also a FSMA requirement that fund participants "do not have day-to-day control over the management of the property, whether or not they have the right to be consulted or to give directions."

Hence, on critical issues where clients' pass-through votes fundamentally conflict with the fund's purpose, Tumelo's platform allows the fund manager to override the vote. Key decisions therefore still sit with the fund and its board of directors. They can do this through the normal proxy voting platform using the "super vote" functionality.

Pre-approving vote policies

Tumelo has partnered with a range of vote policy providers and we look forward to sharing more information on our partner program shortly.

From our full range of vote policies, fund managers review and select a list of "pre-approved" vote policies to make available to their clients which still align with the fund's investment strategy. Institutional clients can also apply their own, pre-existing policies (perhaps from their segregated mandate) to their pass-through votes, if the fund manager allows. This process ensures the fund manager meets their fiduciary duty.

Uniquely, Tumelo also supports clients to override their own vote policy recommendations on an upcoming vote where the client feels they have specific knowledge or goals. This functionality is optional - fund managers can turn it off -, but we know that it's a feature institutional investors love. This feature also means that more clients will opt to follow their fund manager's vote decisions, only feeling the need to intervene on a few key issues throughout the year. We go into detail in this blog post about the key benefits of this set-up.

Conclusion

Clients, especially asset owners, are asking their fund managers for more choice over stewardship decisions and outcomes. Therefore, fund managers must find innovative, efficient and responsible ways to deliver for their clients.

Tumelo's solution enables fund managers to do just that; to offer a product for both institutional and retail clients that has the low cost of a pooled fund, but with the voting flexibility previously reserved only for the largest clients in a segregated mandate - all while fulfilling their fiduciary duty.

To discuss how our product can add value to your organisation, book a demo.

Disclaimer: Information contained within this article should not be considered as professional legal and/or financial advice. Readers will take full responsibility for the use of any information provided.